In India’s rapidly maturing secondary art market, auctions have emerged as critical sites of price discovery, transparency, and market signalling. For collectors, advisors, and institutions alike, understanding the distinction between an auction estimate and a final realised price is essential to interpreting market performance accurately. While these figures are often read together, they represent distinct economic, strategic, and behavioural dimensions of valuation within the Indian art ecosystem.

Auction Estimates: Constructed Expectations

An auction estimate in the Indian market refers to the price range publicly assigned to a work prior to sale, typically expressed as a lower and upper bound, for example, ₹50,00,000 – ₹70,00,000. This range is formulated by auction specialists based on a synthesis of factors: prior auction results for the artist within India and internationally, the scale and period of the work, medium, provenance, exhibition history, condition, and broader market sentiment.

Importantly, estimates are not objective measures of intrinsic value. Rather, they are carefully calibrated expectations designed to balance consignor confidence with bidder participation. In India, where the collector base is still expanding and price sensitivity remains high, estimates are often set conservatively to encourage bidding momentum, particularly for modern masters and mid-career contemporary artists.

Estimates also function as a communication tool. They signal where an auction house believes demand lies at a particular moment, reflecting not only historical data but also curatorial positioning and strategic forecasting.

The Role of the Reserve Price

Closely linked to the estimate, but not publicly disclosed, is the reserve price, the confidential minimum amount below which a work will not sell. In the Indian context, reserves are typically set at or just below the low estimate, ensuring that the work does not sell at a level that could undermine the artist’s market or the consignor’s expectations.

If bidding fails to reach the reserve, the work is “bought in,” a scenario that carries reputational consequences in India’s relatively small and closely observed market. As a result, reserve setting in Indian auctions is often more cautious than in larger Western markets, particularly for artists with limited recent resale histories.

Hammer Price vs. Final Price

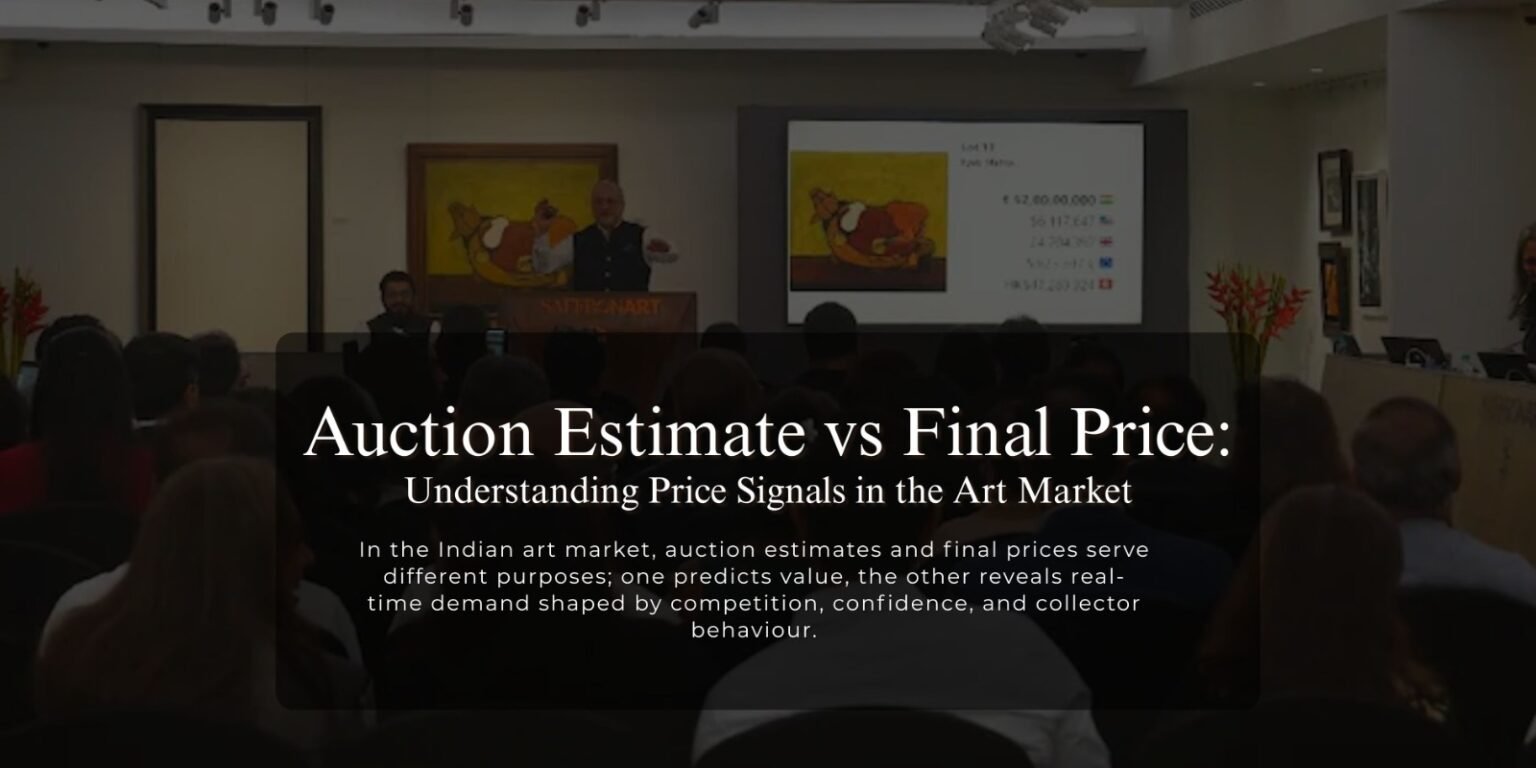

The hammer price is the amount at which bidding concludes and the lot is declared sold. However, this figure does not represent the total cost borne by the buyer. Indian auction houses, including Saffronart, Pundole’s, AstaGuru, and Prinseps, charge a buyer’s premium, typically ranging between 15% and 25%, depending on the price bracket and auction house policy.

For instance, a painting hammered down at ₹1 crore may ultimately cost the buyer ₹1.18–₹1.25 crore once the buyer’s premium is added, excluding Goods and Services Tax (GST), logistics, and insurance. This distinction is crucial, as headlines often report hammer prices, while the true transaction value remains higher.

From an advisory standpoint, the difference between hammer price and final payable price must be carefully factored into acquisition strategy and long-term valuation assessments.

Why Final Prices Exceed or Fall Below Estimates

In the Indian market, divergence between estimates and final prices is shaped by several identifiable forces.

First, competitive bidding plays a decisive role. Works by blue-chip modernists, such as S.H. Raza, F.N. Souza, M.F. Husain, or Tyeb Mehta, often exceed high estimates when multiple collectors pursue rare or historically significant works. Such outcomes reflect scarcity, emotional attachment, and long-term confidence in canonical artists.

Second, strategic under-estimation is common. Auction houses may intentionally set accessible estimates to widen bidder participation, especially among younger collectors. This tactic can result in strong bidding momentum that drives prices well beyond expectations.

Third, market confidence and timing matter deeply in India. A buoyant auction season, increased international interest, or institutional attention can elevate demand, while broader economic uncertainty may temper bidding, causing works to sell closer to or below estimates.

Fourth, data limitations affect accuracy. For artists with thin auction histories, particularly contemporary practitioners, estimates rely on fewer comparables, increasing volatility between expected and realised prices.

Psychology and Social Signalling

Auctions in India are not purely rational transactions. They are social performances shaped by prestige, visibility, and competition. Live and online bidding environments amplify psychological factors: fear of missing out, desire for distinction, and the symbolic value of ownership. These forces can push bidding beyond rational benchmarks, especially when works are perceived as culturally or historically significant.

Conversely, subdued bidding may reflect collective hesitation rather than artistic merit, particularly in moments of market correction.

Price Discovery in the Indian Context

Auction results play a central role in price discovery, offering public benchmarks that influence gallery pricing, private sales, insurance valuations, and institutional acquisitions. However, auctions represent only one segment of India’s art economy. Many significant transactions occur privately through galleries and advisors, often at prices that differ from auction outcomes.

Thus, while auction prices are highly visible, they should be interpreted within a broader ecosystem that includes curatorial narratives, collector relationships, and long-term market development.

Implications for Collectors and Advisors

For collectors, understanding the distinction between estimate and final price is critical to informed participation. Estimates provide guidance, not guarantees. Advisors must contextualise auction data within broader market intelligence, considering provenance quality, artist trajectory, and acquisition purpose.

For galleries and artist representatives, auction outcomes influence perception but do not singularly define value. Strategic engagement with auctions, whether through consignments or market monitoring, requires nuanced interpretation rather than headline-driven reactions.

In the Indian art market, the journey from estimate to final price reveals more than numerical variance; it exposes the complex interplay of expertise, strategy, psychology, and cultural capital. To read auction results critically is to recognise that value is neither fixed nor purely financial, but produced through negotiation, visibility, and collective belief. For those navigating India’s evolving art ecosystem, this distinction is not merely academic, it is foundational.