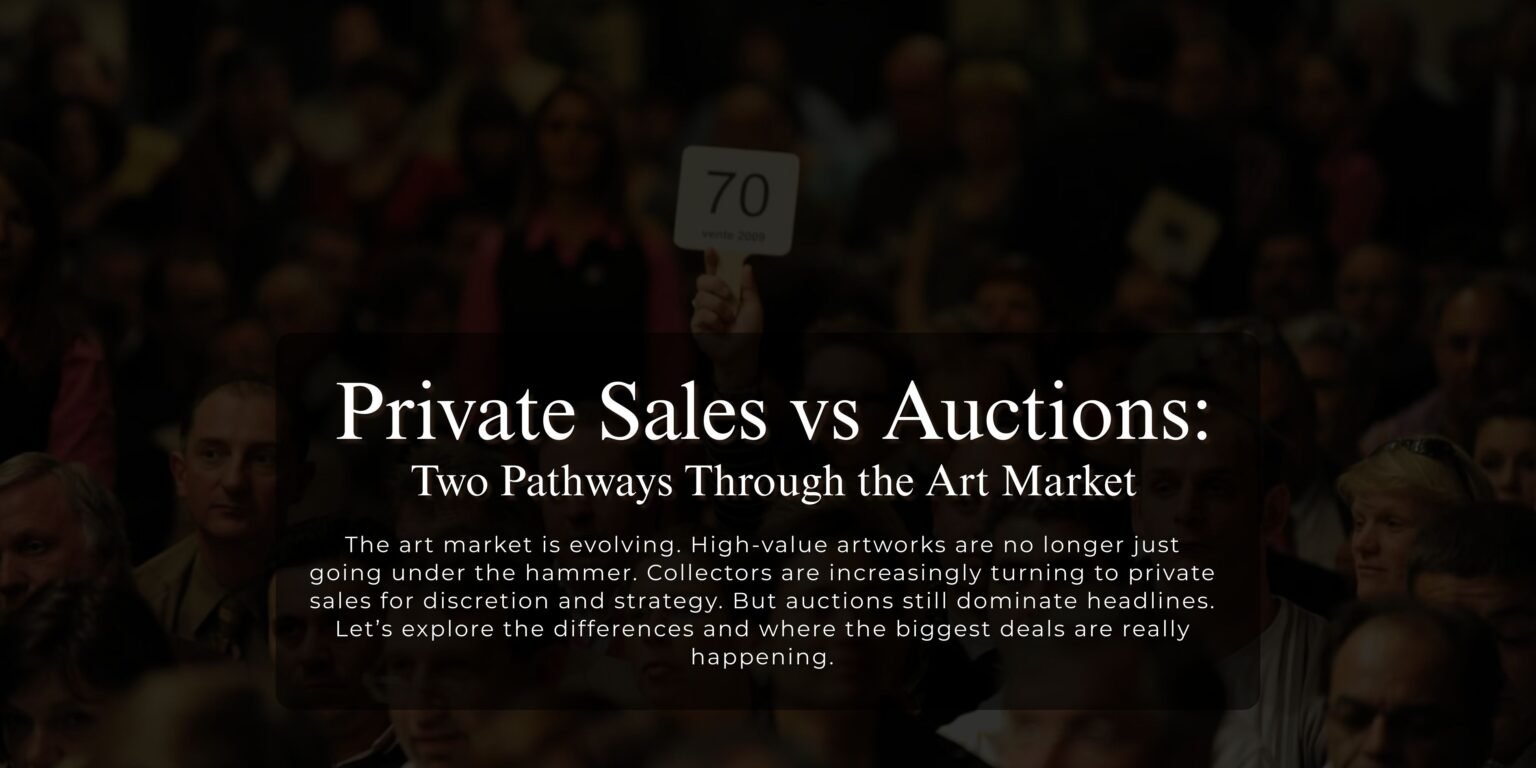

In the architecture of the global art market, transactions occur primarily through two mechanisms: public auctions and private sales. Although both serve as conduits for buying and selling artworks, they operate according to fundamentally different economic, social, and institutional logics. For collectors, advisors, and galleries, understanding these distinctions is essential, not merely for navigating transactions, but for interpreting how value is constructed and sustained within the art ecosystem.

Within contemporary art advisory practice, the question is no longer simply where art should be bought or sold, but how each mechanism shapes perception, pricing, and cultural legitimacy.

Auctions: Theatre, Transparency, and Market Benchmarks

Public auctions represent the most visible segment of the art market. Conducted by major houses and regional firms alike, auctions function as highly orchestrated events in which artworks are sold to the highest bidder through competitive bidding. The process is structured around pre-published estimates, catalogues, and a defined sale date.

One of the most significant features of auctions is price transparency. When a work sells publicly, its hammer price and buyer’s premium are typically reported in databases and the press. These results often become reference points for future valuations. In fact, auction outcomes frequently establish the benchmark prices for artists within the secondary market.

This public visibility can have powerful consequences. If bidding competition is strong, the resulting price may significantly exceed expectations, reinforcing the artist’s market prestige. Auctions therefore offer the possibility of dramatic value escalation driven by competitive demand.

However, this transparency also introduces risk. If a work fails to sell or achieves a price below its estimate, the result becomes permanently recorded. Such outcomes can affect perceptions of an artist’s market strength. For this reason, consignors must weigh the reputational implications of auction results before bringing works to sale.

Auctions also involve substantial transaction costs. Buyer’s premiums can exceed 20-25 percent of the hammer price, while sellers typically pay commissions that may range from 5 to 15 percent or more depending on the value and the auction house.

Despite these costs, auctions remain indispensable because they generate price discovery, a process through which market demand publicly determines an artwork’s value.

Private Sales: Discretion and Negotiated Value

Private sales represent a contrasting mode of transaction. In this framework, artworks are sold discreetly through galleries, dealers, advisors, or the private sales departments of auction houses. Instead of open bidding, prices are negotiated directly between buyer and seller.

The defining feature of private sales is confidentiality. Unlike auctions, private transactions generally leave no public record of the price paid or the parties involved. For collectors seeking discretion, particularly those dealing with high-value works, this privacy can be highly attractive.

Another advantage lies in flexibility. Because private sales are not bound to a specific auction calendar, transactions can occur at any moment when buyer and seller agree. This allows collectors to act strategically rather than waiting for scheduled auction seasons.

Transaction costs are also often lower. Private dealers typically charge commissions that are significantly smaller than those associated with auctions, and fees can often be negotiated depending on the relationship between the parties.

Yet the very discretion that makes private sales appealing can also create challenges. Without publicly recorded prices, market transparency diminishes. Buyers must therefore rely heavily on expert advisors, market data, and trusted intermediaries to ensure fair valuation.

Visibility vs Targeted Access

Another distinction between the two channels lies in how artworks reach potential buyers.

Auctions provide broad exposure. Catalogues, marketing campaigns, and global bidding platforms ensure that artworks are seen by a wide audience of collectors and institutions. This visibility can drive competition and potentially elevate prices.

Private sales, by contrast, involve targeted placement. Dealers and advisors often approach a curated group of collectors whose interests align with a particular artwork. While this reduces competitive pressure, it allows transactions to occur within a carefully managed network of relationships.

For galleries representing living artists, such targeted placements are often essential. By controlling where works are placed and who acquires them, galleries can cultivate collectors likely to preserve the artist’s reputation and support their long-term career trajectory.

The Role of Auction Houses in Both Markets

Interestingly, the boundary between auctions and private sales has become increasingly fluid. Major auction houses now operate substantial private sales divisions alongside their public auctions. These departments broker discreet transactions for collectors who prefer confidentiality or who wish to sell works outside the competitive environment of the auction room.

Private sales have therefore become an important revenue stream for auction houses. In some cases, institutions aim to increase the proportion of turnover derived from private transactions, reflecting growing collector demand for bespoke services.

This hybrid model illustrates the evolving structure of the art market: rather than competing channels, auctions and private sales now function as complementary mechanisms within a broader transactional ecosystem.

Strategic Considerations for Collectors

From an advisory perspective, the choice between auctions and private sales depends on several factors.

Collectors seeking maximum market exposure and potential price escalation may prefer auctions, where competitive bidding can drive values upward. Conversely, sellers wishing to avoid public scrutiny, or to protect a work from the risk of failing to sell, often favour private negotiations.

Buyers, too, must weigh the dynamics carefully. Auctions offer transparent pricing but can encourage emotional bidding wars that push prices beyond initial expectations. Private sales provide calmer negotiations but require deeper knowledge of market valuations.

In practice, seasoned collectors often move fluidly between both channels, using each according to strategic needs.

Private sales and auctions represent two distinct yet interdependent structures within the art market. Auctions generate public benchmarks, establishing visible records of value through competitive bidding. Private sales, by contrast, offer discretion, flexibility, and personalised negotiation within curated networks of collectors and advisors.

For art advisory practices, the critical task lies not in choosing one model over the other but in understanding when each is most effective. The art market ultimately thrives on a balance between transparency and discretion, spectacle and strategy.

In this delicate interplay, auctions provide the theatre of price discovery, while private sales quietly shape the relationships and negotiations that sustain the market behind the scenes.